How To Write Effective Credit Report Dispute Letter

As a provider of affordable credit repair,we get asked a lot of questions regarding

writing credit report dispute letters, such as “How do I write a dispute letter?”

or “How do I do it myself?”,

So this article will cover the contents of How To Write Effective Credit

report dispute letter, and what it looks like so you can construct one of your own.

You should be aware the credit reporting agencies are massive corporations and have spent a

You should be aware the credit reporting agencies are massive corporations and have spent a

lot of time and money doing their job, which is selling your credit report data.

They also have spent a lot of money learning how to avoid credit repair letters and your credit report dispute letters.

Don’t be surprised if your first efforts fail, or if

the credit reporting agencies don’t respond,- or – if they stall you with some nonsense,

or claim they verified an item when they did not.

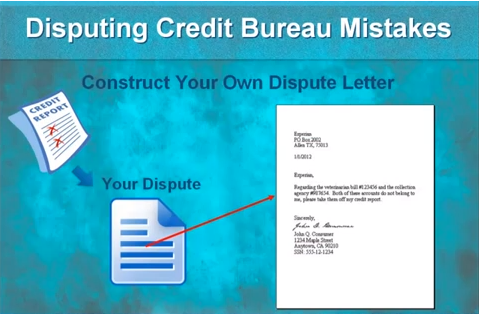

So lets start by saying you went to annualcreditreport.com,and got a free copy of your credit report

sent to you. When you looked at it, there were 2 accounts you know don’t belong to

you, lets say an account with a local veterinarian,and a collection company collecting the veterinarian

account.

Start your letter by knowing who you are sending the letter to, date it, and include their

address.

Then get right into it and be direct, list the name and account number of the items you

are disputing.

Then sign, and date your letter, but you also need to include your identifying information,

such as name, address and social security #.

It’s that simple! Make sure your penmanship is readable, then make a copy for your own

records and mail your signed letter to the bureau. Sometimes its helpful to include a

photocopy of your drivers license.

How to write effective credit report dispute letter

If your letter has too many irrelevant details and sounds like a story, then you are doing

it wrong.

Don’t write a letter that tells a sad story; “Those accounts belong to my ex wife, it happened

when I stayed too long at the bar, when I got home she was MAD and had her stuff packed

up – and said she wanted a DEEE-VORCE, then she STOLE my truck and ran over her OWN dog

on the way out!, Well – I did take the poor dog to the vet but it was HER dog and HER

vet bill!”

Don’t do that! Keep it simple and get right to the point: “It’s not my account, please

take it off my credit report.” So if you get frustrated, don’t waste a lot of time on

it Don’t call them on the phone. Don’t dispute it online, – you will waste time, and you

won’t get what you want. If it doesn’t work, just hire a credit repair services professional. It’s affordable and will save you time.

So there you have it, a quick tutorial on how to write effective credit report dispute letter.

Thank you for reading, and good luck.

The next piece is how much you owe as a percentage of the

The next piece is how much you owe as a percentage of the And second, it can cause your ratio of

And second, it can cause your ratio of